Deja Vu All Over Again: OPEC and Friends Agree To Cut Production

May 31, 2017

The Organization of the Petroleum Exporting Countries (OPEC) and a group of high producing allies, including Russia, have agreed to extend their combined 1.8 million barrels per day (MMbpd) production cuts for nine months starting in July. The decision was widely expected, however, and appears to have been priced into the market. Brent crude prices actually dropped 4% after the announcement was made, falling to $51.90 per barrel, as some market participants were hoping for deeper and/or longer cuts to production.

From January through June of this year, OPEC has cut output by 1.2 MMbpd, with the other nations lowering production by 0.6 MMbpd. Compliance with the first cuts has been surprisingly high, 95% for OPEC and 65% for non-OPEC nations. The agreement is better than the alternative of no cuts and should help balance a global oil market that is still oversupplied by as much as 1.5 MMbpd.

Yet, the effects will be limited. After all, the agreement is the same as the first one, which failed to shrink global crude oil stockpiles to OPEC's target level, seeking a drawdown from a record high of 3 billion barrels to the five-year average of 2.7 billion. The goal has been undermined by weak demand, robust OPEC exports, and quickly rebounding U.S. crude production.

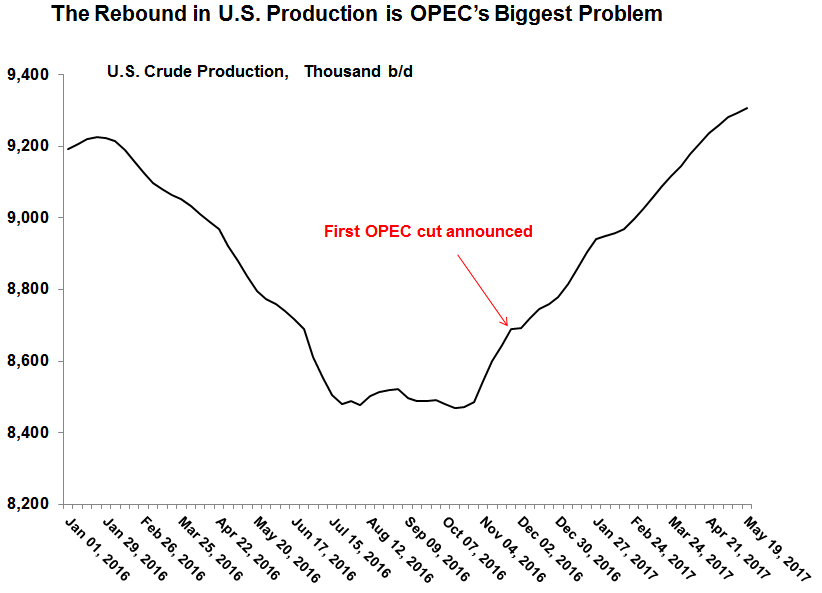

Indeed, the real dilemma for OPEC is that the bump in prices from the first cut allowed U.S. shale oil producers to lock-in hedges at higher rates, thus increasing output. And the halving of prices since 2014 to just $50.00 per barrel today forced U.S. drillers to become more efficient, mastering such techniques as tighter well spacing, longer laterals, and multi-pad drilling. Many U.S. producers can now make a profit when prices are just $40.00 per barrel. The impressive declines in breakeven costs have given shale companies more sources of capital to finance the drilling of new wells, including hedging, bank and private loans, and high-yield bonds.

Since OPEC’s first cut was announced at the end of November, U.S. crude production has increased 8% to over 9.3 MMbpd, and the Energy Information Administration projects another 8% gain to a record 10.0 MMbpd by the end of next year. Moreover, other key nations are slated to continually increase production, namely Brazil (pre-salt), Canada (tar sands) Nigeria, and Libya, the latter two being OPEC members but exempt from the production cuts.

Ultimately, oil prices will struggle to break out of their current range around $50.00 a barrel until the market is convinced exports are falling and stockpiles are drawing down. This could take at least a year. For example, the U.S. has a record 5,720 drilled but uncompleted (DUC) wells ready to be unleashed onto the market as prices rise, and if prices would ever reach $60.00, the country could surge output by over 1.0 MMbpd.

Goldman Sachs has recommended that OPEC try to flip the oil market from contango (where futures prices are higher) into backwardation (where futures prices are lower) by making it clear that members will up production again after the nine month agreement and once inventories rebound. A backwardated oil market would make selling currently stored crude more attractive while also making it more difficult for U.S. producers to hedge future output. Goldman, however, might be overestimating the power that OPEC still holds.