Blog

Published: December 28, 2016

U.S. Northeast Gas Plays Getting Critical Pipeline Relief

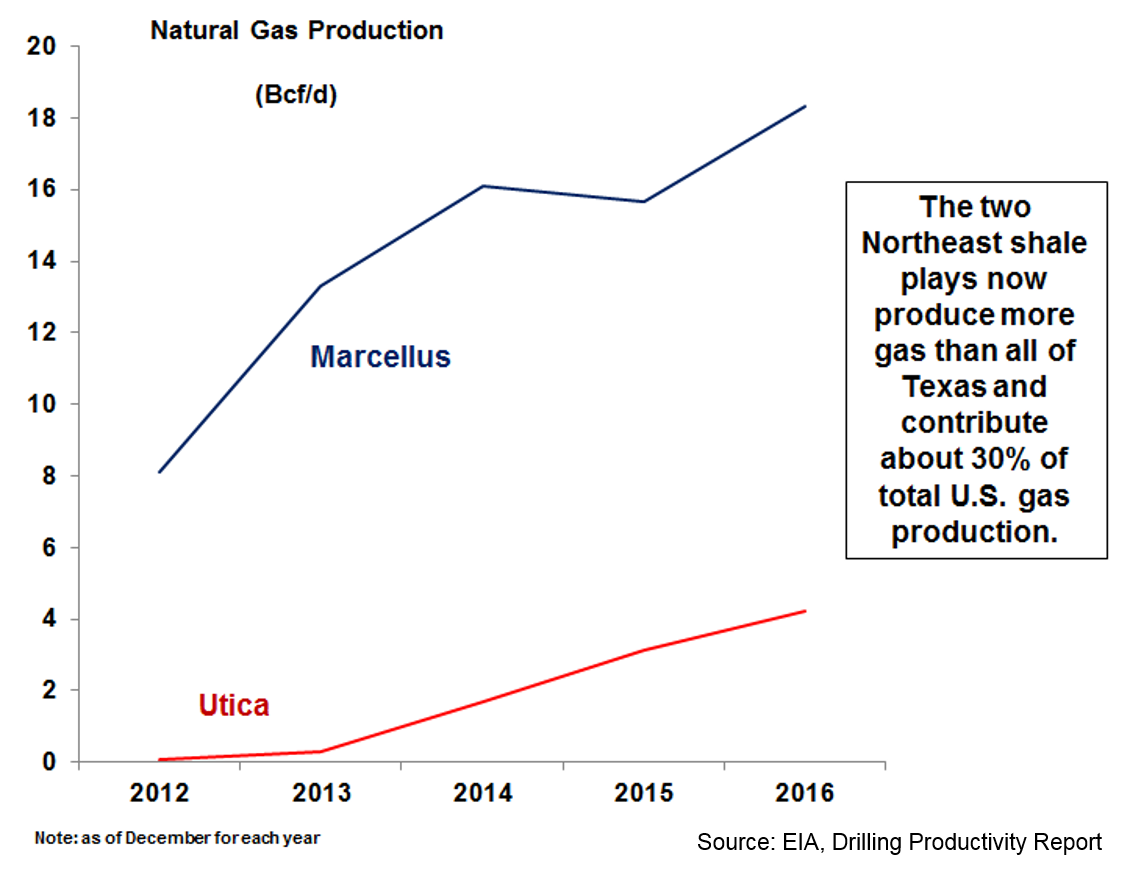

Even since the price collapse started 2014, natural gas production in the Marcellus has increased nearly 15% to 18.3 Bcf/d, with output in the neighboring Utica up 130% to 4.1 Bcf/d. These two northeast shale plays are almost single handedly reversing the U.S. gas market to flow more north to...

U.S. Northeast Gas Plays Getting Critical Pipeline Relief

December 28, 2016

Even since the price collapse started in 2014, natural gas production in the Marcellus has increased nearly 15% to 18.3 Bcf/d, with output in the neighboring Utica up 130% to 4.1 Bcf/d. These two northeast shale plays are almost single handedly reversing the U.S. gas market to flow more north to south, east to west.

Yet, more takeaway capacity in the northeast is critical for new supply to reach customers: a lack of pipelines means lower prices for producers, and production can get shut-in. At trading points in and around the Marcellus/Utica, gas often trades $1 or more below the Henry Hub national benchmark in Louisiana.

U.S. Northeast Gas Production Continues to Surge

Looking forward, the northeast has a number of new midstream projects in various stages of regulatory approval expected to come online by 2018. Although the environmental pushback against new fossil fuel infrastructure is gaining strength, new gas pipeline and reversal projects could soon add 16-18 Bcf/d out of the region:

The Rover pipeline could transport 3.25 Bcf/d to Ohio, West Virginia, Michigan, and on into the Dawn Hub in Ontario, Canada. The new pipeline and its related facilities to Defiance, Ohio are hoped to be in-service by mid-2017, with an in-service date to Vector/Dawn Hub by November.

The Leach Xpress seeks to add 1.5 Bcf/d of takeaway capacity to serve customers on the Columbia Gas and Columbia Gulf pipeline systems, having a targeted in-service date of the second half of 2017.

The Rayne Xpress project will augment Leach Xpress and add 0.6 Bcf/d in takeaway capacity from the Columbia Pipeline system to markets along the Gulf Coast. Rayne is expected to be placed into service in the fourth quarter of 2017.

The Nexus Gas Transmission project will deliver 1.5 Bcf/d of supplies to markets in northern Ohio, southeastern Michigan, the Chicago Hub, and the Dawn Hub in Ontario. Nexus has a targeted completion date of fourth quarter of 2017.

The Mountaineer XPress will transport 2.7 Bcf/d to markets on the Columbia Gas Transmission system, including to customers in western West Virginia, TCO Pool, and other mutually agreeable points. Columbia anticipates initiating construction in the fall of 2017, with a targeted in-service date of October 2018.

The Mountain Valley pipeline would run at least 2 Bcf/d south from the MarkWest Energy Mobley complex in northwestern West Virginia to southern Virginia. Moutain Valley is expected to be fully in-service during the fourth quarter of 2018.

The Atlantic Coast pipeline would have a capacity of 1.5 Bcf/d to run gas from Tyler County, West Virginia south to Virginia on the way to North Carolina. Construction is expected to begin in the fall of 2017.

The Atlantic Sunrise expansion project would transport about 1.7 Bcf/d to markets in the Mid-Atlantic and southeastern U.S. The pipeline should be in-service by 2018.

The PennEast pipeline will transport 1 Bcf/d from northeastern Pennsylvania to Transco’s pipeline interconnect in Mercer County, New Jersey. An in-service date of November 2017 is anticipated.

The Algonquin Incremental Market (AIM) project will add 0.345 Bcf/d of Northeast shale gas to the highly capacity-constrained New England market. On November 1, Spectra placed part of AIM into service, and the remainder of the project should be completed this month. Another Spectra project to increase capacity on Algonquin, the Access Northeast, could bring an additional 925,000 Bcf/d of capacity into the region by the fourth quarter of 2018.

After reversing flows on its eastern-most sections of its Zone 3 segment in mid-2014, Tallgrass Energy’s Rockies Express Pipeline (REX) expects to ramp up its 0.8 Bcf/d Zone 3 Capacity Enhancement project by the end of this year.

Currently, the total operating receipt capacity for producers to deliver gas onto REX is nearly 4.3 Bcf/d, compared to the 1.4 Bcf/d that was online in August 2015. Competing against more supplies from western Canada, more bi-directional capacity on REX will give Midwest customers even more access to Marcellus/Utica gas.

The U.S. switch to a northeast gas center is now being reflected in futures and physical trading contracts and the prices those contracts are pegged against. Companies are now buying much more gas linked to the Marcellus pricing points than historically could have been imagined. As northeast takeaway capacity grows, gas prices spreads with the Henry Hub benchmark in Louisiana continually narrows.

In addition, the switch to the northeast not only reflects the boom in shale gas production, but also a growing recognition that pricing all U.S. gas off a single hub no longer makes sense. Accounting for the bulk of the 55% increase in U.S. gas production by 2040, some believe that the growth in Marcellus and Utica shale will install pricing hubs in Philadelphia, where there’s open access to domestic and foreign markets, and at Pittsburgh’s Dominion South Point, where in some recent months physical gas volumes traded have been 70% higher than the day-ahead volumes at the Henry Hub market.

So, looking at the North American gas market as a whole, in less than a decade, we will have installed an entirely new system where western Canadian supplies struggle to compete with U.S. northeast gas into the Midwest and eastern Canada, and gas from the northeast is flowing through Louisiana into Texas and then down the coast to LNG export terminals and pipelines to Mexico.